Selling gold bars will incur a tax. personal income tax is one of the most significant changes of Personal Income Tax Law 2025 This regulation, recently passed by the National Assembly, marks a major turning point in the management of the precious metals market, shifting from a free market to a framework of strict tax controls similar to other investment assets.

According to experts at MAN – Master Accountant Network, applying a tax rate of 0.1% on the value of each transaction not only aims to increase government revenue but also serves as an effective regulatory tool to curb speculation and manipulation of gold prices. In the context of an economy moving towards transparency, understanding the tax roadmap and calculation methods is crucial for both individual investors and gold trading organizations.

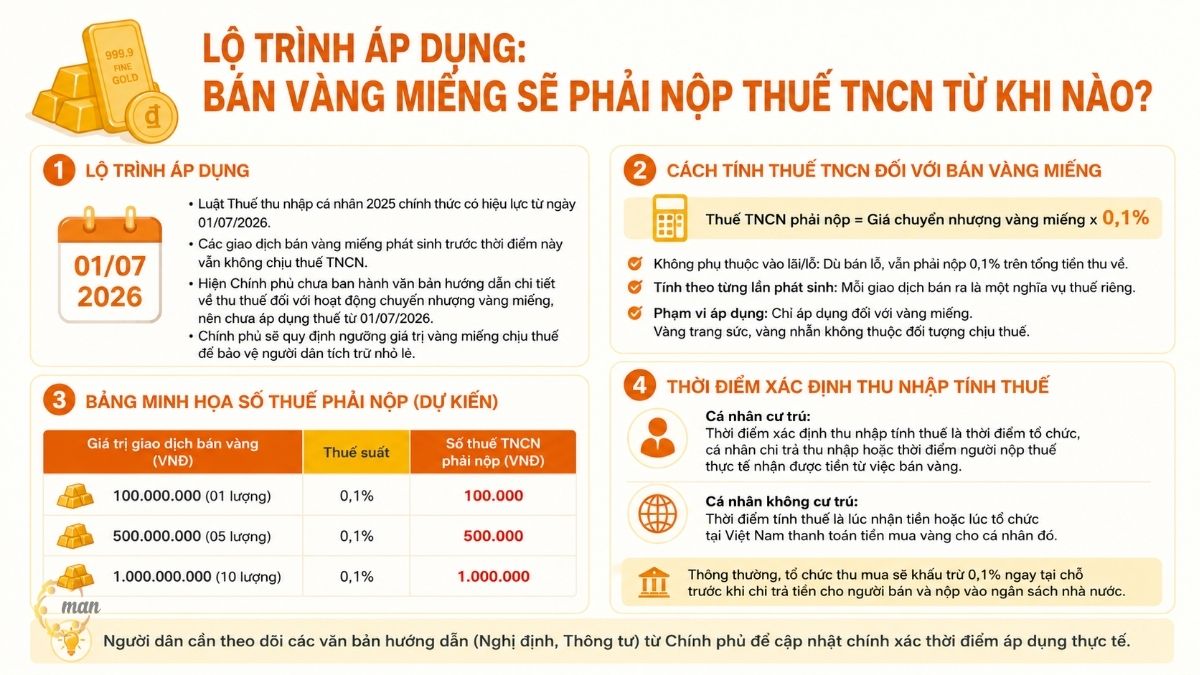

Bán vàng miếng sẽ phải nộp thuế TNCN từ khi nào?

Based on the provisions of Article 29 of the Personal Income Tax Law 2025, the entire law officially comes into effect from this date. 1/7/2026. This means that transactions occurring before this time will still be conducted according to current regulations (not subject to personal income tax when selling gold bars at retail).

Hiện Chính phủ chưa quy định chi tiết về việc thu thuế đối với hoạt động chuyển nhượng vàng miếng tại dự thảo Nghị định mà cần có văn bản quy định tổng thể về chính sách thuế và quản lý thuế đối với hoạt động kinh doanh, mua bán vàng. Do đó, hiện vẫn chưa áp dụng việc thu thuế chuyển nhượng vàng miếng từ ngày 1/7/2026.

However, under Clause 10, Article 3 of the new Law, income from the transfer of gold bars has been officially listed as "Taxable Income". The government is also empowered to specify the tax threshold for gold bars to ensure that it does not put pressure on individuals who hoard small amounts for welfare purposes.

Tax rate of 0.1%: Calculation method and specific illustrative examples.

Many people wonder whether this tax is calculated on profit or on the total selling price. According to Clause 2, Article 19 and Article 27 of the Personal Income Tax Law 2025, the sale of gold bars is subject to personal income tax based on the following formula:

|

Personal income tax payable = Transfer price of gold bars x Tax rate 0.1% |

Key features of this calculation method:

- Regardless of profit/loss: Even if you sell gold at a price lower than the purchase price (resulting in a loss), you still have to pay 0.1% on the total amount received.

- Calculated per transaction: Each sales transaction generates a separate tax liability.

- Scope of application: This tax applies only to "gold bars". Gold jewelry and gold rings are not subject to this tax.

| Gold sales transaction value (VND) | Tax rate | Amount of personal income tax payable (VND) |

| 100,000,000 (1 tael) | 0,1% | 100.000 |

| 500,000,000 (05 taels) | 0,1% | 500.000 |

| 1,000,000,000 (10 taels) | 0,1% | 1.000.000 |

Time of determining taxable income for gold bars

Determining the correct tax assessment time helps taxpayers and tax authorities avoid legal disputes. The Personal Income Tax Law 2025 stipulates:

- For resident individuals: The time of determining taxable income is the time when the organization or individual pays income to the taxpayer, or the time when the taxpayer actually receives the money from the sale of gold.

- For non-resident individuals: Similarly, the tax calculation time is when the money is received or when the organization in Vietnam pays the individual for the gold purchase.

Typically, at authorized gold shops or banks that trade in gold bars, the tax deduction is done on the spot. The purchasing organization is responsible for deducting 0.1% before paying the seller and remitting it to the state budget.

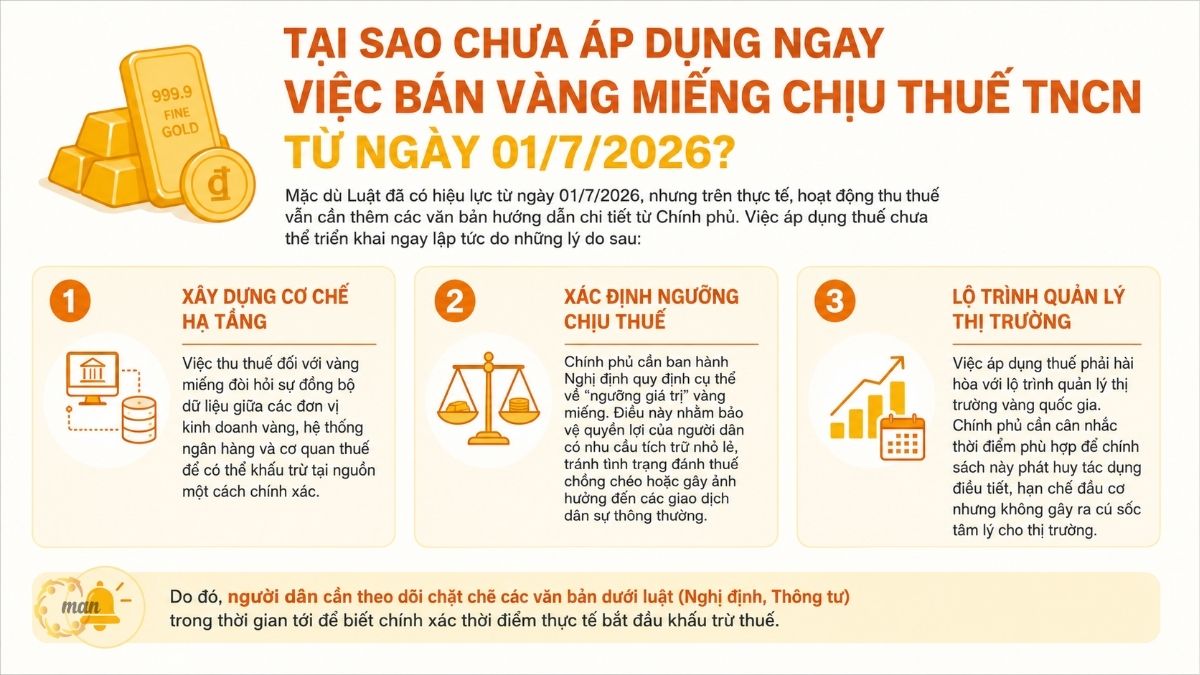

Tại sao chưa áp dụng ngay việc bán vàng miếng chịu thuế TNCN từ ngày 01/7/2026?

Mặc dù Luật đã có hiệu lực từ ngày 01/7/2026, nhưng trên thực tế, hoạt động thu thuế vẫn cần thêm các văn bản hướng dẫn chi tiết từ Chính phủ. Việc áp dụng thuế chưa thể triển khai ngay lập tức do những lý do sau:

- Xây dựng cơ chế hạ tầng: Việc thu thuế đối với vàng miếng đòi hỏi sự đồng bộ dữ liệu giữa các đơn vị kinh doanh vàng, hệ thống ngân hàng và cơ quan thuế để có thể khấu trừ tại nguồn một cách chính xác.

- Xác định ngưỡng chịu thuế: Chính phủ cần ban hành Nghị định quy định cụ thể về “ngưỡng giá trị” vàng miếng. Điều này nhằm bảo vệ quyền lợi của người dân có nhu cầu tích trữ nhỏ lẻ, tránh tình trạng đánh thuế chồng chéo hoặc gây ảnh hưởng đến các giao dịch dân sự thông thường.

- Lộ trình quản lý thị trường: Việc áp dụng thuế phải hài hòa với lộ trình quản lý thị trường vàng quốc gia. Chính phủ cần cân nhắc thời điểm phù hợp để chính sách này phát huy tác dụng điều tiết, hạn chế đầu cơ nhưng không gây ra cú sốc tâm lý cho thị trường.

Do đó, người dân cần theo dõi chặt chẽ các văn bản dưới luật (Nghị định, Thông tư) trong thời gian tới để biết chính xác thời điểm thực tế bắt đầu khấu trừ thuế.

Why is it necessary to require personal income tax to be paid on the sale of gold bars?

The application of the 0.1% tax is considered a "management fee" to enable the State to obtain accurate data on the flow of money in the gold market. From the perspective of MAN – Master Accountant Network's auditing and tax consulting services, this regulation brings the following values:

- Transparency in transactions: Restrict informal transactions and promote the issuance of electronic invoices in the gold trading business.

- Anti-speculation: Although the tax rate is small (0.1%), it will directly impact groups of people who "speculate" on gold with large volumes and high frequency.

- Macroeconomic stability: Reduce the appeal of hoarding gold bars and direct social capital towards more efficient production and business investment channels.

Những lưu ý quan trọng để chuẩn bị cho quy định bán vàng miếng chịu thuế TNCN

Trong thời gian chờ đợi các hướng dẫn chi tiết, cá nhân và nhà đầu tư nên chủ động chuẩn bị để đảm bảo tuân thủ pháp luật:

- Phân biệt rõ loại hình vàng: Quy định hiện tại tập trung vào “vàng miếng”. Các loại vàng trang sức, vàng nhẫn phục vụ nhu cầu làm đẹp, quà tặng không thuộc đối tượng điều chỉnh của chính sách này.

- Lưu trữ chứng từ giao dịch: Việc giữ lại hóa đơn, chứng từ mua bán vàng từ các đơn vị uy tín là thói quen cần thiết. Điều này giúp cá nhân chứng minh nguồn gốc tài sản và giá trị giao dịch trong tương lai.

- Cập nhật thông tin từ nguồn chính thống: Tránh hoang mang trước các luồng thông tin không chính xác trên mạng xã hội. Hãy thường xuyên theo dõi Cổng thông tin điện tử của Chính phủ hoặc cơ quan thuế.

- Tham vấn chuyên gia: Đối với nhà đầu tư nắm giữ danh mục vàng miếng lớn, việc tham khảo ý kiến từ chuyên gia kế toán, tư vấn thuế là cần thiết để lên kế hoạch tài chính phù hợp, đảm bảo sự minh bạch trước những thay đổi của Luật Thuế thu nhập cá nhân 2025.

Kết luận: Việc bán vàng miếng chịu thuế TNCN là một lộ trình tất yếu để minh bạch hóa thị trường. Dù mức thuế suất không quá cao, nhưng sự chuẩn bị kỹ lưỡng từ phía người dân và doanh nghiệp sẽ giúp quá trình chuyển đổi này diễn ra thuận lợi và hạn chế rủi ro pháp lý.

Conclude

The imposition of a personal income tax of 0.11% on the sale of gold bars, effective from July 1, 2026, is an irreversible policy in Vietnam's roadmap for improving its tax system. Although the tax rate is not excessively high, the declaration and deduction process will require thorough preparation from gold trading businesses and a good understanding from the public.

To ensure compliance with the law and optimize personal or business financial plans during this transition period, clients should seek support from professional services. MAN – Master Accountant Network is proud to be a leading provider of such services. auditing services, tax accounting services, tax consulting services, tax settlement services and tax reporting services In-depth expertise. We are committed to helping businesses and individuals prepare accurate and timely tax reports, minimizing legal risks arising from the new regulations of the Personal Income Tax Law 2025.

Service contact information at MAN – Master Accountant Network

- Address: Số 19A, Đường 43, Phường Tân Thuận, TP. Hồ Chí Minh

- Mobile/Zalo: 0903 963 163 – 0903 428 622

- E-mail: man@man.net.vn

- Google Business Profile: Xem Google Business Profile của MAN – Master Accountant Network

- LinkedIn Founder: Xem hồ sơ LinkedIn của chuyên gia Lê Hoàng Tuyên

Phụ trách sản xuất và kiểm duyệt nội dung chuyên môn bởi: Ông Le Hoang Tuyen – Sáng lập viên (Founder) & CEO MAN – Master Accountant Network, Kiểm toán viên CPA Việt Nam với hơn 30 năm kinh nghiệm trong lĩnh vực Kế toán, Kiểm toán, Thuế và Tư vấn Tài chính doanh nghiệp.

Frequently Asked Questions about whether selling gold bars is subject to personal income tax.

No. The law only stipulates that the sale of gold bars is subject to personal income tax. Gold rings and gold jewelry are currently not subject to this tax.

According to Clause 9, Article 3, income from inheritance is subject to tax only if the property is registered for ownership/use. Gold bars are currently not subject to registration like real estate, so inheriting gold bars may not be subject to personal income tax under this category. However, when you sell that gold, you will be subject to a tax of 0.11% on the selling price.

The law mandates the government to set specific threshold values. Experts predict there may be a tax-free limit for small transactions (e.g., under 20 million or 50 million VND) to support small-scale savings by individuals. If I sell plain gold rings, do I have to pay the 0.1% tax?

If I inherit gold bars, will I have to pay tax?

At what value does taxation begin?

{kind=link}

{kind=link}