Circular 152/2025/TT-BTC Officially issued on December 31, 2025, replacing Circular 88/2021/TT-BTC, this document marks a turning point in the financial management of small businesses. It standardizes the legal framework based on the latest Accounting Law and Tax Management Law, helping business owners access a professional and transparent management system.

Compliance with Circular 152/2025/TT-BTC is mandatory to ensure tax benefits and avoid legal risks. With the implementation schedule starting from January 1, 2026, business households need to understand the changes in personnel, documents, and accounting systems to operate a streamlined and standardized accounting system.

Subjects and personnel performing accounting duties according to Circular 152/2025/TT-BTC

The circular clearly stipulates the autonomy of the representative in organizing the accounting system. The head of the household can keep records themselves, arrange personnel, or hire professional accounting services appropriate to the actual scale of the household.

The breakthrough lies in the relaxation of family ties. The representative can appoint relatives (spouse, parents, children, siblings) to work as accountants or concurrently hold positions such as warehouse manager or cashier. This regulation helps business households save costs while still ensuring reliability and tight internal control.

In addition, individual businesses can hire qualified accounting service providers. Outsourcing helps ensure accuracy, timely updates on changes in electronic invoicing and online tax filing policies, and minimizes errors in financial management.

Regulations on the storage of accounting documents and records according to Circular 152/2025/TT-BTC

Document archiving under Circular 152/2025/TT-BTC is flexible in line with the digital transformation trend. Business households have the right to choose to archive documents using traditional paper copies or electronic means to optimize space and facilitate inspections.

The minimum retention period for accounting documents is 5 years. Sales and purchase invoices, in particular, must comply with the retention period stipulated by current tax laws. This is an important regulation aimed at facilitating long-term tax reconciliation and protecting the legal rights of business households.

| Criteria | Paper archives | Electronic storage |

| Convenience | Watch it live, but it takes up space. | Saves space, fast search |

| Durability | Easily damaged by the environment. | Good security is ensured if there is a backup system. |

| Expense | High printing and warehousing costs. | Initial IT infrastructure costs |

| Duration | Minimum 5 years (Circular 152/2025/TT-BTC) | Minimum 5 years (Circular 152/2025/TT-BTC) |

Accounting system for business households not subject to tax according to Circular 152/2025/TT-BTC

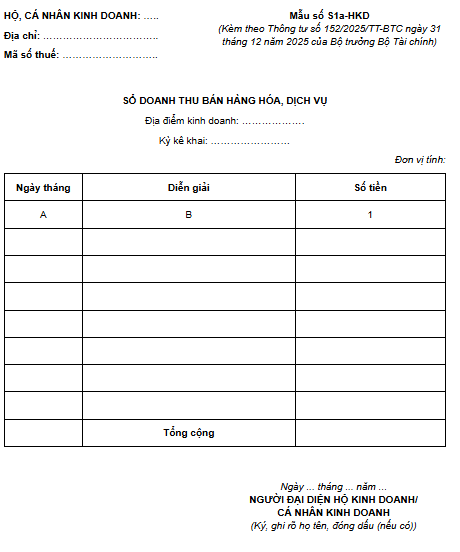

For businesses with low revenue, they are not subject to the regulations. VAT and personal income tax, Circular guiding the use of the simplest ledger form to track revenue thresholds, as a basis for determining tax obligations when they arise.

The main notebook template is Sales Revenue Register for Goods and Services (Form S1a-HKD). This ledger helps record daily transactions visually, without requiring complex debit and credit entries, maximizing convenience for self-managed small businesses.

The recording method in form S1a-HKD includes:

- Date column: Record the actual time the transaction occurred.

- Explanation column: Briefly describe the type of goods or services offered.

- Amount column: Record the actual monetary value received from the customer.

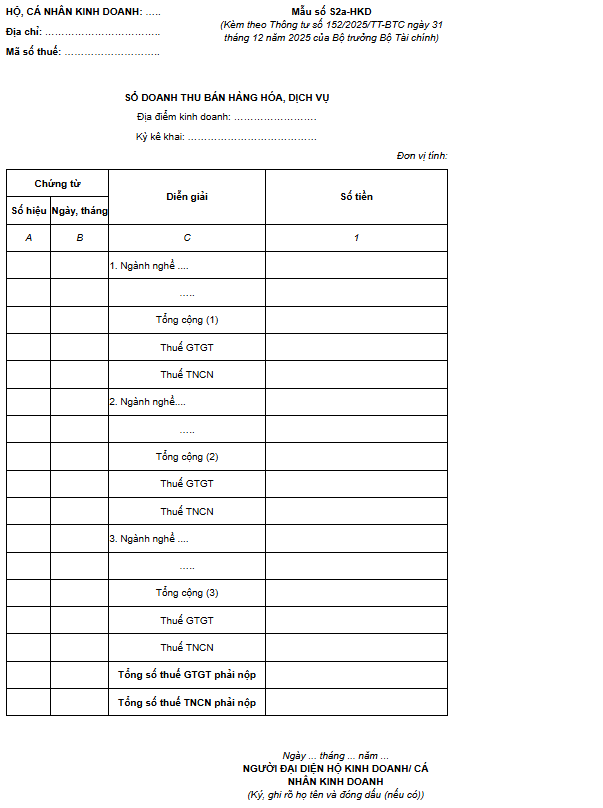

Accounting for taxpayers paying taxes at a rate of 1% tax on revenue, as per Circular 152/2025/TT-BTC.

Taxpayers subject to a % rate on revenue must use invoices and related documents as the basis for determining revenue. Using valid documents helps to ensure transparency of data and shorten the time spent dealing with tax authorities.

The applicable ledger template is Sales Revenue Register for Goods and Services (Form S2a-HKD). This ledger allows for the classification of revenue into industry groups with the same VAT and personal income tax rates (%), helping to accurately calculate the tax payable each period.

| Occupational groups | Revenue | VAT rate % | VAT payable |

| Distribution and retail of goods | 100.000.000 | 1% | 1.000.000 |

| Services, construction (excluding contracting) | 50.000.000 | 5% | 2.500.000 |

| Production and transportation (including contracting) | 80.000.000 | 3% | 2.400.000 |

| Other business activities | 20.000.000 | 2% | 400.000 |

Using the S2a-HKD form helps business households easily compare data with the tax authority's information system, ensuring accuracy in fulfilling their obligations to the state budget.

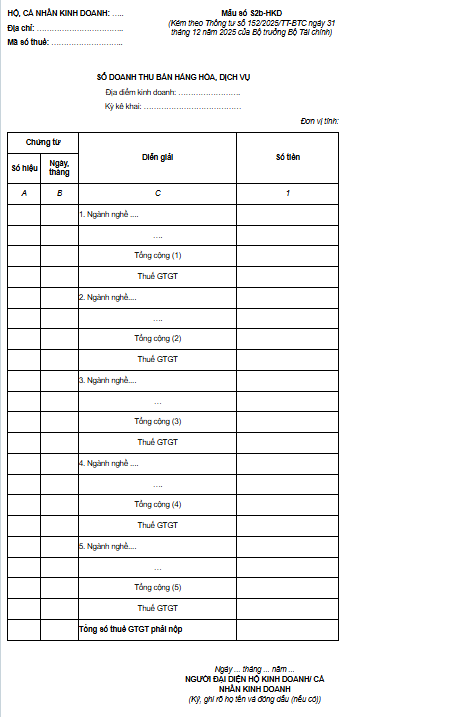

Accounting for households paying personal income tax on taxable income according to Circular 152/2025/TT-BTC

For individuals and household businesses applying the method of paying personal income tax on taxable income, Circular 152/2025/TT-BTC mandates the establishment of a complete accounting system to accurately determine revenue, deductible expenses, and taxable income.

According to regulations, deductible expenses must be supported by legitimate grounds, including:

- Invoices and supporting documents are valid in accordance with the law on invoices.

- List of goods and services purchased without invoices (according to the prescribed form)

- Documents related to actual production and business expenses incurred.

To meet the above requirements, business households must open and maintain complete records of the four types of accounting books as stipulated in Article 6 of Circular 152/2025/TT-BTC, specifically as follows:

Sales revenue register for goods and services

This notebook is for use Record all revenue generated during the period., include:

- Sales revenue

- Revenue from providing services

- Other revenue related to business operations

Revenue is tracked. each time it occurs, as a basis:

- Determine taxable revenue

- Compare with the issued invoice.

- To help determine the VAT rate (if applicable).

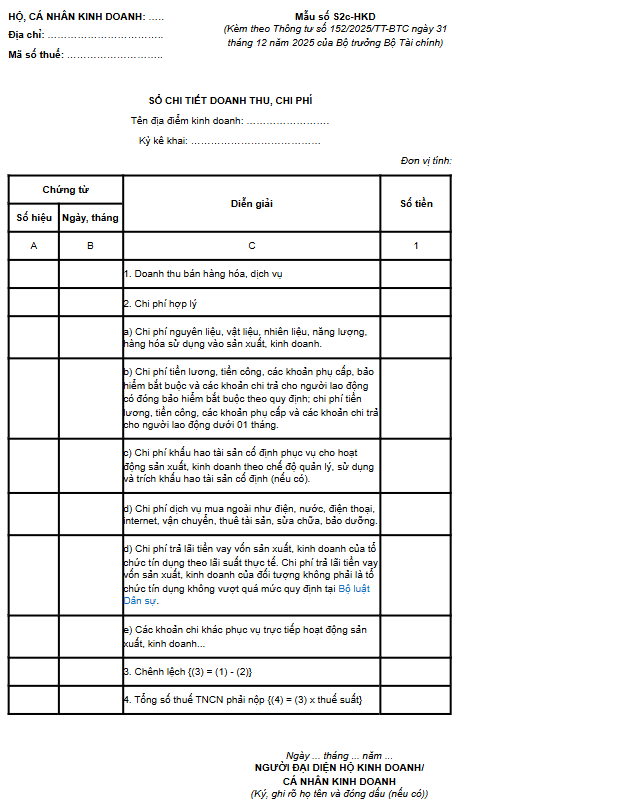

Detailed ledger of revenue and expenses

This is most important notebook to determine taxable income, reflecting:

- Actual revenue

- Reasonable and legitimate expenses are deductible.

The expenses recorded include:

- Cost of raw materials and goods

- Labor costs

- Fixed asset depreciation costs

- Interest expense related to business operations.

- Other legitimate production and business expenses

This notebook is the direct basis for calculating personal income tax payable according to the formula:

Taxable income = Revenue – Deductible expenses

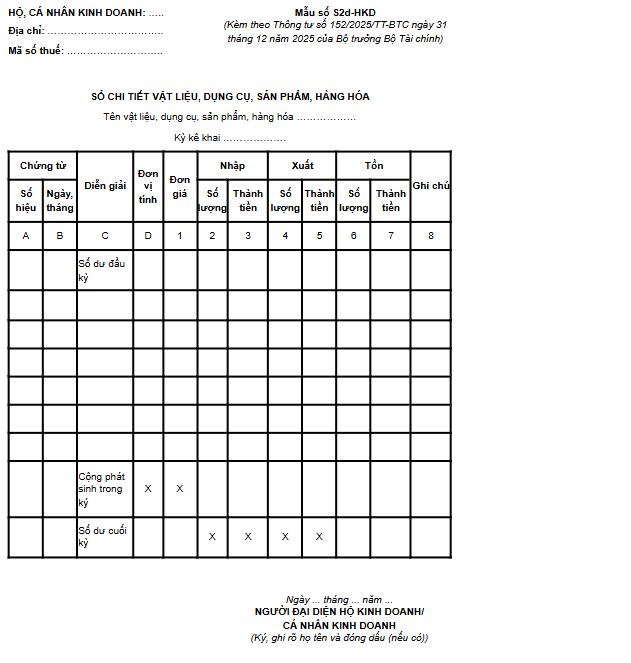

Detailed register of materials, tools, products, and goods.

The notebook is used for... managing inventory, import, export, and stock levels., include:

- Raw materials

- Tools, products

- Goods for sale

The value of goods sold is determined as follows weighted average method, help:

- Accurately reflect the cost of goods sold.

- Avoid cost discrepancies.

- To provide evidence of reasonable expenses when settling taxes.

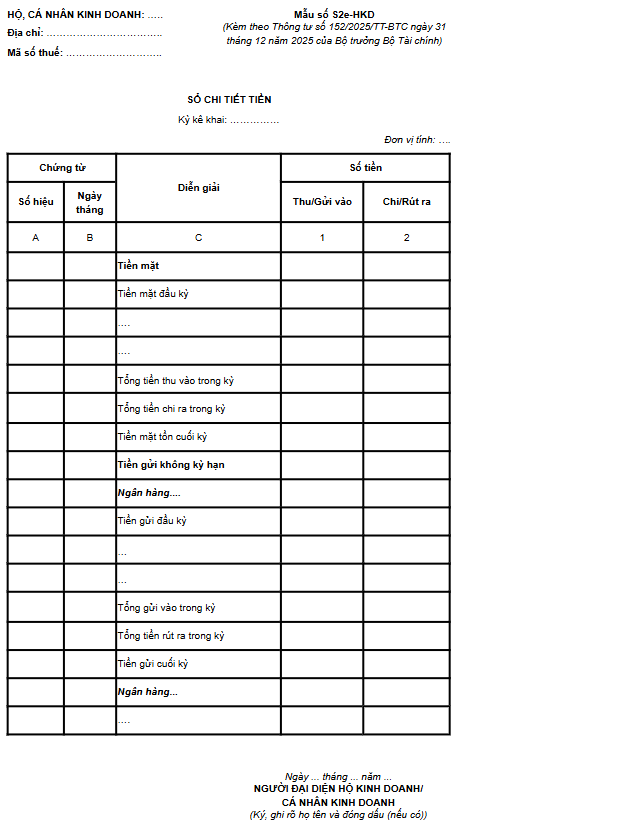

Cash register

This log is for tracking all currency fluctuations of household businesses, including:

- Cash

- Demand deposit

The information in the register helps:

- Control cash flow (inflow and outflow).

- Compare with recorded revenue and expenses.

- Demonstrate financial transparency during a tax audit.

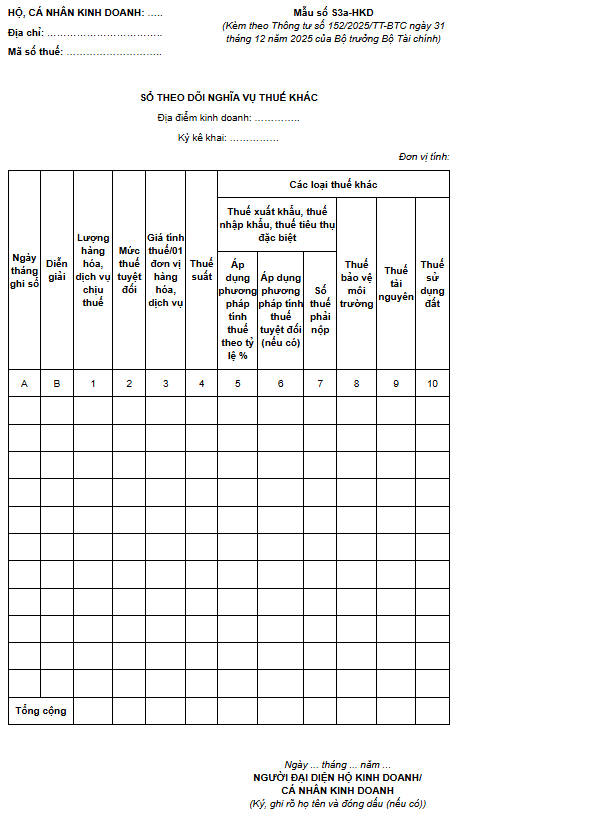

Accounting for other types of taxes (Import-Export, Resource, Land Tax, etc.) according to Circular 152/2025/TT-BTC

In cases where a business household has specific activities subject to other taxes (export tax, import tax, special consumption tax, resource tax, environmental protection tax, land use tax), the Circular requires the use of additional resources. Other Tax Obligation Tracking Register (Form No. S3a-HKD).

This ledger helps to track the details of taxable goods, taxable value, and the corresponding tax calculation method (% rate or absolute amount). Complete record-keeping helps businesses systematically control all arising budgetary obligations.

Conclude

Circular 152/2025/TT-BTC is an important legal framework that helps business households standardize their financial management. Strict adherence to the regulations not only ensures tax safety but also helps to increase transparency in financial data, leading to more effective access to bank loans.

If you need support in implementing an accounting system according to Circular 152/2025/TT-BTC, let MAN – Master Accountant Network be your partner. We provide solutions. full tax accounting, Professional and optimized. Contact MAN today!

Service contact information at MAN – Master Accountant Network

- Address: No. 19A, Street 43, Tan Thuan Ward, Ho Chi Minh City

- Mobile/Zalo: 0903 963 163 – 0903 428 622

- Email: man@man.net.vn

Content production by: Mr. Le Hoang Tuyen – Founder & CEO MAN – Master Accountant Network, Vietnamese CPA Auditor with over 30 years of experience in Accounting, Auditing and Financial Consulting.

Frequently Asked Questions about Accounting for Household Businesses under Circular 152/2025/TT-BTC

Yes (Article 3). Household businesses are allowed to supplement or modify the form to suit their needs, provided that the core information (register name, date of creation, signature of the representative) is included.

This Circular takes effect from January 1, 2026, completely replacing Circular No. 88/2021/TT-BTC.

Yes. The circular stipulates that business households still use these ledger forms to track and reconcile the amount of tax payable according to the tax authority's notice (Article 3, Clause 4). Can sole proprietorships independently modify accounting ledger forms?

When does Circular 152/2025/TT-BTC take effect?

If using electronic invoices, is it still necessary to record them in a ledger?

{kind=link}

{kind=link}